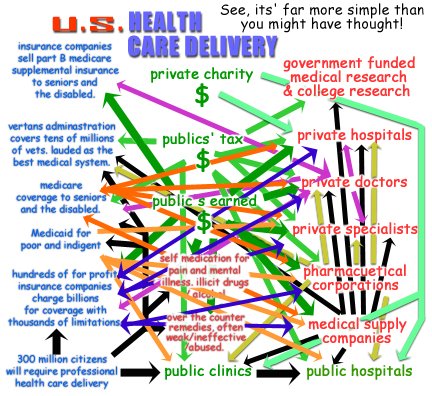

Sorry the article below does not begin to describe the details of the illustration above. However, each line represents the taking or giving of services and or money to and from each of the entities shown. Each line represents the way we are dealing with the inevitable struggle of health care delivery and financing that every single American will have to deal with.

Sorry the article below does not begin to describe the details of the illustration above. However, each line represents the taking or giving of services and or money to and from each of the entities shown. Each line represents the way we are dealing with the inevitable struggle of health care delivery and financing that every single American will have to deal with.1860, Growing Town, U.S.A.:

George Common seeks opportunity, as he sits and thinks, nursing a jug of whiskey.

“Gee, as I look around town I see that about half of my fellow townspeople go into debt with old’ Doc Wilkins, every time they sick. Hmmm, how can I capitalize on this problem? How can I exploit this condition of depravity to my gain? I’ve got it! I’ll collect a pool, of sorts, of their money, like say One Hundred bucks per year! Since most of my fellow community members don’t get sick within a year, heck most of them go several years without anything going wrong, I’ll have more than enough to pay their medical bill to Doc Wilkins, take a good share for myself and expand the scam, err the business.”

Thus a new type of insurance company was born. Of course selling insurance was nothing new at this time, Lloyds of London was offering Casualty and Loss insurance already for centuries. For all new business ventures there has to exist a need to fill, a condition to exploit. For success there also must exist; a disciplined and consistent methodology of profit which is too advantageously provocative to turn away from.

Medicine was primitive in the nineteenth century, but still leaps and bounds beyond the centuries past. Surgery had advanced, arterial manipulation had begun to save lives, the meaning of a fever had begun to be understood, and clean surgical method was being practiced. So people who visited the town doctor began to live beyond their diseases. Although the odds of their deaths were still greatly against them, it was getting better, and this made the sale of medical insurance financially feasible. Because a person might live, he she would live to see the debt acquired post medical treatment. In the urban centers the doctors were charging more where wealth existed, and when a contagion broke-out, it spread to many. For the doctors, charging the wealthy more allowed for a quasi compensated volunteerism towards the poor, who were afflicted with any number of air and blood born illnesses. Health insurance was not advantageous here in the cities of the eighteenth and nineteenth centuries, because the poor couldn’t pay anything, and the wealthy and middle class could easily afford to pay cash.

As the industrial revolution rose to fruition health insurance grew with it, but known as Sickness Insurance, which often shared its title with Disability Insurance, so that health treatment claims were directly related to the person’s inability to further work. This restriction meant the patient paid for any illness not related to work or ability to work further for his employer. This also meant that selling policies what’s adverse risks only came into play if the insured policy holders work was threatened, was clearly profitable.

The 1950s, and the nice doctor next-door your mother wanted you to be:

In the television 1950’s (not to be confused with reality in that decade) your town doctor might just live next door to you, sharing a driveway perhaps. You see Doctor J. Atomic when you get your mail, and you chat over the backyard fence. His car is a Chevy, just like yours. He and his wife are on the PTA, he did a term on the city council. His house is a three bedroom, just like yours, he borrows stuff from your garage, you and his wife play Bridge together on Thursday nights, a month ago you all got too drunk and a huge yelling fight ensued, causing the game to end early. But you all quickly forgave each other a few days later. Doctor Atomic charges Twenty dollars an hour for office visits, and he doesn’t care if you have insurance or not. Sure, it’s nice to have a patient with insurance, but most folks in town pay any debt they have to him anyway. After all, it’s not a large town, and he’s so nice, so relaxed, and you guessed it: he looks amazingly like actor Robert Young, circa 1954.

2006:

Doctor J. Modern is not that doctor of nearly fifty years ago. He doesn’t live next door anymore. Not really. You know he or she is in “that” house. But that house is now two hundred yards away. The lawn has an iron fence and a gate with security cameras. He drives a BMW with its windows so dark you can’t even see him. His kids are shuffled off to a private school somewhere on the outside of town. You know someone who goes to him, at a privately owned clinic on the fifth floor of a mirrored glass cube of a ten story building in an office park. Doctor J. Modern is a General Practitioner – that’s what the “sees generally all ailments” doctors are called now. It takes about two months to get an appointment with him and folks in town will leave their own grandmothers hanging-out on a street corner to make that appointment on time. He golf’s as much as he can but you can’t golf with him because the country club he goes to is $12,000 per year.

New Costs:

Consumers are demanding their insurance companies meet more of these ever increasing costs. Competition between the insurance companies is but a moot concept, as premium prices, deductibles, and issued claim amounts vary only in the names and amount dispersals. Insurance industry conventions and secret meetings in the Bahamas between the top executives, “insure,” that premiums are nearly identical, that pay-outs are chocked-off through the use of numerous excuses, by using billions of dollars to employ thousands of lawyers to fight legitimate claims in courts, and the use of very fine print in initial contracts. Television and magazine advertising show middle aged wives and mothers looking into the camera, with an almost tear in their eyes and saying, “I don’t know what we would have done without Nationwide Premium Health, they really were there for my family when we needed them.” Stoking the fire of fear in the consumer public the insurance industry makes uses of the greatest known propaganda tactic to “insure,” their ever lasting survival.

Enter Medicare, 1965:

The insurance industry was just beginning to realize the incredible potential of selling health insurance as more and more citizens annually had been buying insurance. Better, having health insurance provided as a “benefit,” through one’s employer was bringing millions into the fold of the insurance industry. But the decades long debate over covering the poor and indigent and seniors with government subsidized health insurance had won out in favor of a new program called Medicare. Signed into law on June, 30th, 1965, as part of President Lyndon B. Johnson’s Great Society initiatives. The corporate lobbying by Health Insurance providers that went into trying to stop this legislation was probably the beginning of non-war related corporate lobbying as it is known today. In 1972 the program was extended to include the disabled of any age, and those using the Social Security Income program for household income. Practically overnight the nation insured 30 million seniors and disabled citizens. At the time the premium for Part B Medicare, office visits, hospital stays and etc., was $3 per month. No longer did little old ladies have to eat cat food so they could afford to pay an insurance company valued at $200 million, $25-100 per month for coverage. In the 1970s Health Maintenance Organizations began cropping up, often formed by groups of doctors, or private investors seeking their piece of the health care pie. Soon, Medicare became available to these HMOs. Health Insurance premiums rose like an Apollo launching during the late 1970s-1980s, it seemed that Medicare was just too good to allow those insurance companies their “sky is the limit,” growth.

Medicare and the Provider’s Nightmare:

For the hospital managing to stay solvent financially is all they want to do. For Dr. J. Modern, its different, because his family and house is an expensive lifestyle he is not willing to reduce, he wants to be rich enough to be able to quit the practice when ever he wants.

Now, in 2006, a lot of providers have started to refuse to accept Medicare patients. Since its inception, out payments to providers have been gradually cut almost every year. Payments to providers have reached a point where from the viewpoint of the professional provider almost any private insurance is far better than Medicare. An entire segment of our Congress has hated Medicare since its beginnings. They despised the whole socialist sounding dogma of President Johnson’s Great Society. We may never know but it appears as if the Republicans wanted a nation of haves and have nots. The have nots working and stagnating without upward mobility, always serving the haves. The conservatives strongly feel that getting sick and using medical care should cost a person money, his or her own money, not hand-outs. So attack Medicare and Medicaid they did. Taking little nibbles year after year like small carnivorous fish in a creek that Americans have to walk through. Often the cuts were concessions with the other side of the congressional isle, deals, back rubbing. One can be assured that insurance company lobbying, fighting to reduce the effectiveness of their greatest competitor, had a lot to do with those budget cutting decisions.

Even though Medicare has kept itself solvent year after year, with solvency forecast between four and twenty eight years throughout its history. It was cast as a failure by the Republicans. They broadcast complaints from sought after individual stories, of little old ladies being denied services having resulted from the very programs Medicare was forced to cut back on, due to their ruthless budgeting priorities. Oddly the complaint that most galvanized public discord to agree with the Republicans was the stories of the long waits on the telephone, just to ask a question.

Private insurance monthly premiums increased two and three fold, just within the 1980s. The excuse from the insurance companies was those blasted diagnostic tests. Yes they were expensive. But that never explains the increasing profits of the insurance companies. After all, if preventing a monetary loss while still providing the quality insurance services that their customers expected, had been their goal all along. They could never have gone public and sold shares, their offices would not be skyscrapers, their executive bonuses would not be among the highest in the world.

Recipients responsibility for Medicare Part B, was now $85 per month mid 2006. Wages and or Social Security incomes from Medicare recipients never did catch-up to this type of cost increase. The only group of individuals who may have seen an increase of 28 times their original rate of pay, might be the insurance company executives.

Behind the office park where Dr. Modern’s office is located (along with the offices of fifty other doctors and medical specialists) is the hospital. The facility was built in the early 1980’s at a cost of around $42 million. In today’s costs of construction and medical equipment, including all the latest diagnostic equipment, computers, monitors, cameras and etc, that same capacity hospital would cost more than $200 million. A new hospital would never pay for itself at that start-up cost. That cost would have to be passed on to the consumer in any way possible, often desperately. The existing hospital built twenty five years back, has not escaped the inflation of medical costs, it had to upgrade everything just like all the other health care providers and hospitals. Additionally the nations’ pharmacopoeia has grown by thousands of percent just since the early 1980s.

Hospital managers are under constant pressure to find the money. The Health Care Financing Administration in Washington D.C., which manages the Medicare financing and reports to the public, has had to cut way back on services, on which specific types of illnesses and hospital stays it would pay what percentage for. Cut backs are directly in proportion to the budget reductions from the U.S. Congress. Sadly the politicians get away with it with dirty public relations tricks. The most common is the annual budget increase, but not enough to meet the increase in annual patient needs, including the one million or so new patients added to the population, just from being born each year. This allows the President and Congressional conservatives (who hate government) to proclaim they have increased Medicare spending. To the applause of little old Republican ladies in the audience.

In the late 1980s and reaching the height of popularity by 2000 was the Medicare over-treatment and thus over-billing. This could be done in the wide open. Medicare had reached a point where its merit in terms of dollars paid, far surpassed by private insurance companies. Smiling Nurses who are on the front line of the arrangement are oblivious to what they are allowing. After all, it’s the doctor’s orders and it’s not their call. So, a seventy-two year old man with a peptic ulcer spends four nights in a private hospital room. He is prescribed a fancy new pharmaceutical, which comes from the hospital’s own pharmacy and is priced at $18 per capsule. It’s the same pill the Canadian’s are getting from the same manufacturer for just $2 per capsule. The Nurses document his recovery, from a crying and wincing dependant old man, to an upright in bed, watching television, laughing and pinching a Nurses rear-end. All within 18 hours of his arrival. He was ready to go home then. But the doctor ordered Magnetic Resonance Imaging of his esophagus, causing a wait delay, then the diagnostician’s delay. This type of testing, and delaying has allowed the hospital to bill his Medicare over $18,000 for the four day stay. But modern Medicare, after all the years of cuts, is only going to pay $11,000. A private insurance company would have paid all of this amount, but it also would have utilized %17-%28 of its income from customer premiums to process, and delay, and argue costs, and short shrift any provider it can. Amounts and percentages are all relevant in a system that allows the give and take of funding for services, unchecked, with sky is the limit boundaries.

Medicare used to have enough fraud inspectors to police the system in an adequate manner. Now there are less than 100 inspectors for approximately 3000 hospitals, a hundred thousand doctors, and so on. Getting away with bilking Medicare is almost a sure thing. Medical supply companies have seen exponential growth since lobbying efforts have won them the ability to charge Medicare for all kinds of previously prohibited equipment. Motorized wheelchairs are selling like dairy milk as those companies are now advertising full Medicare financing. Obese people who develop extreme lower back pain are getting doctors to sign off on legitimate claims of disease rather than BBQ ribs, so they can travel from the bed to the recliner to watch television.

Medicare had not failed. The idea of Medicare, and Medicaid, has not failed. What has failed is our representatives ability to protect Medicare from those who despise its very ideology. Our representatives have also failed to protect Medicare from the fraud that followed this nibbling at the ankles destruction of the program. The only type of laws our entire country seems to respect is those delineated in the United States Constitution. Therefore knowing what we would do to a new health care program, I suggest we write any new Universal Healthcare, into the Bill of Rights as an Amendment. Violating that amendment with fraud or insufficient funding, would be a violation of the Civil Rights of all.

“Frivolous Lawsuits!”

Dr. Modern complains about his liability insurance costs, he’ll gladly tell any of his patients that he spent “over eighty thousand dollars last year,” on liability insurance. If he only knew why he pays so much he might be furious; the same company that provides his liability insurance, also takes premiums money from his patients for health insurance and from citizens who drive for auto insurance. Could it be that the books of one insurance company don’t care which category of income makes what, so long as the income is positive and the stock prices go up and the executive bonuses are bigger than the year before? Yes exactly, whether their profits come from Dr. J. Modern and his brethren or all those millions of worried hypochondriacs, or even all those millions of drivers who buy auto insurance, its all the same account on someone’s desk on one of the top floors in those tallest buildings in the world.

Why does Doctor J. Modern think that his liability insurance is destroying his ability to be fruitful at his medical practice? Some politicians and pundits have been telling him that the whole problem is “frivolous lawsuits,” desperate patients suing their surgeons for silly reasons, like leaving a scar. Although less than %2 of all dollars spent on health care delivery in the U.S. is spent on litigation, one would not know it listening to Doctors like J. Modern.

Another financial secret the insurance companies, would rather Doctor J. Modern not know, is that they play with his and everybody else’s money in the stock market, in bonds and securities. In a study by the Government Accounting Office has found that “lower-than-expected investment income for 15 large insurers between 2000 and 2002 probably played an important role in their rate-setting.” (Rosman, “Background Paper: Medical Malpractice in Crisis,” p.10).

Similarly, an analysis by the American Academy of Actuaries also found that liability insurers’ investment income decreased as a percentage of premiums between 1995 and 2001, and it suggested that each one percent decrease in interest rates would require insurers to increase premiums 3 to 4 percent to offset the reduced investment income. (Schactman, Doonan, and Rosman, “Policy Brief: Medical Malpractice in Crisis,” Council on Health Care Economics and Policy, (May, 2003), p. 5).

A fourth hidden factor driving liability rates skyward is the monopolization of insurance companies. Mergers and acquisitions from one company by another, decrease competition. In fact it is often a motivation for buying-out the holdings of another insurance company. With less competition, whether they had cooperated in pricing or not, premiums for all categories of insurance can drive upwards by the remaining companies still in the market. (Rosman, “Background Paper: Medical Malpractice in Crisis,” p. 4).

Nearly all states, and recently the federal government have capped pain and suffering (the worst part of having the wrong leg chopped off) to just $250,000 in total. No longer can a judge or a jury decide (as our Constitution says they should) what is proper and just punishment for a guilty party, based upon suffering, be it lifelong or a couple years. What’s the rest of your life ruined by a busy surgeon, or a sponge stuck in your gut, worth? One or two million dollars at least? No, $250,000. Running around our system of justice to appease doctors whose real complaint should be with the insurance companies, is not the answer.

Lobbyists have everything to do with every measure passed or not in our congress, at least for the last twenty five years about health care. Using our premium dollars against us, the health insurance companies have been one of the most active and high spending lobby’s in the history of Capital Hill. It was lobbyists that convinced Republican lawmakers that the high cost of liability insurance was due to “frivolous lawsuits.” And the people were fooled too, not realizing that not one lawsuit gets past the bench and on to a trial without the judge deciding it has merit or is frivolous. The insurance industry lobbyists convinced the people that it is because they “ . . have to hire all these lawyers,” that premiums are so high for the poor doctors, “ . . we have to make it up somewhere!” These measures totally deflected all heat from the insurance industry, saved to continue to reap the profits.

While Doctor J. Modern pays $80,000 annually to have decent liability coverage, on the other side of the country some doctors are paying $180,000 annually, and they have the same insurance company. Super bilking of premiums from Beverly Hills to subsidize Suburban Town, NY is another hidden secret they don’t want these doctors to know about. It has been three years since the Republicans passed the new caps on Pain and Suffering damages to patients, and Dr. J. Modern hasn’t see his rates go down one penny, in fact they went up last year by %3. He remembers the Republican president speaking to a crown in front of an HMO in Tennessee about how frivolous lawsuits destroying our health care system. He supported him, because he was addressing an issue dear to his wallet.

When citizens elect persons who loudly exclaim the failures of government. Then those persons enter government, enjoy their congressional pay and health insurance, then they set out to prove their original contention.

In 1994 a Republican senator, speaking on the floor, displayed a diagram that was portrayed as a satire of the proposed health care reforms offered by then President Bill Clinton. He displayed a spaghetti plate network of squiggly lines to indicate to his constituents that the proposal was just the kind of government bureaucracy that he and his ilk came to Washington to destroy.

Avoiding large bureaucracy is almost impossible. Streamlining bureaucracy is possible as proven by the Clinton administration during the 1990s, when that office under the supervision of then Vice President Al Gore, cut nearly 400,000 government positions during his tenure, and maintained and even strengthened our government’s abilities.

We are the government. A government of the people, by the people, and for the people. In government all are accountable. That doesn’t mean all get caught for mismanagement and corruption, but all in the public trust are in one way or another, at some time eventually, accountable. That is a huge difference between government and the private sector. Secondly; one’s goal is to make money, the other’s goal is to meet the goal as public servants.

One excellent definition of a Democratic government is: “ . . the coming together of people or groups of people, to accomplish as a whole what they could not, or would not , as individuals or as groups of individuals.” This describes a power that has made America strong and beneficial for most for two centuries. Anyone who can agree with that the premise within this definition, must then realize that everything we are doing in terms of our health care delivery, is not working. It is a proven failure and individuals and groups of individuals have consistently failed to change the system.

So we use the power of our government once, again as in Social Security, Medicare and Medicaid, and a basket of other programs designed because their needs could not be met without the democratically combined power of the whole of nation. We can use this power once again to create a universal health care payment and delivery system which covers every citizen.

This process is best defined as a “Single Payer System.” One payer in one location with one agent for a case, one check for a doctor, one payment for a hospital. No quibbles, no bickering, no thousands of lawyers to litigate their way out of their employers promises. Pharmaceuticals acquired wholesale for the best possible price to the taxpayers. Inspectors in every city and most small cities, ready to catch provider based fraud such as over billing and over treatment. The price gouging will stop, no more aluminum canes for $49.99, no more $8,000 hospital fitted reclining beds that don’t talk. A man with a esophageal ulcer won’t get an MRI, he’ll get an optical scan, and his heartburn pills won’t cost him $18, probably only $2. Clinics can be built by the thousands, specializing in preemptive healthcare, and birth to death maintenance of the body. The clinics alone will eventually save billions of dollars over the old system. An irony is, these cost saving measures on the provider side, are all the kinds of “suggestions,” health insurance companies have been peddling to providers for decades, and having success. Would you rather have your accountable government chose how to save your own money (your taxes), or have some secret coalition of health insurance companies influence those cuts, you may or may not notice the next time you go to your doctor or the local hospital? The cuts under a Single Payer system would be readily announced and even voted upon by a council appointed by the president and approved by congress. Cuts by the insurance companies are secretive, creeping deceptively, and only allow them to make more money. Private insurance premiums never go down, so the savings are the executive’s alone.

Visit SiCKOCure.org to learn more and become a part of the struggle for real universal health care.